Special Offer

Highlights

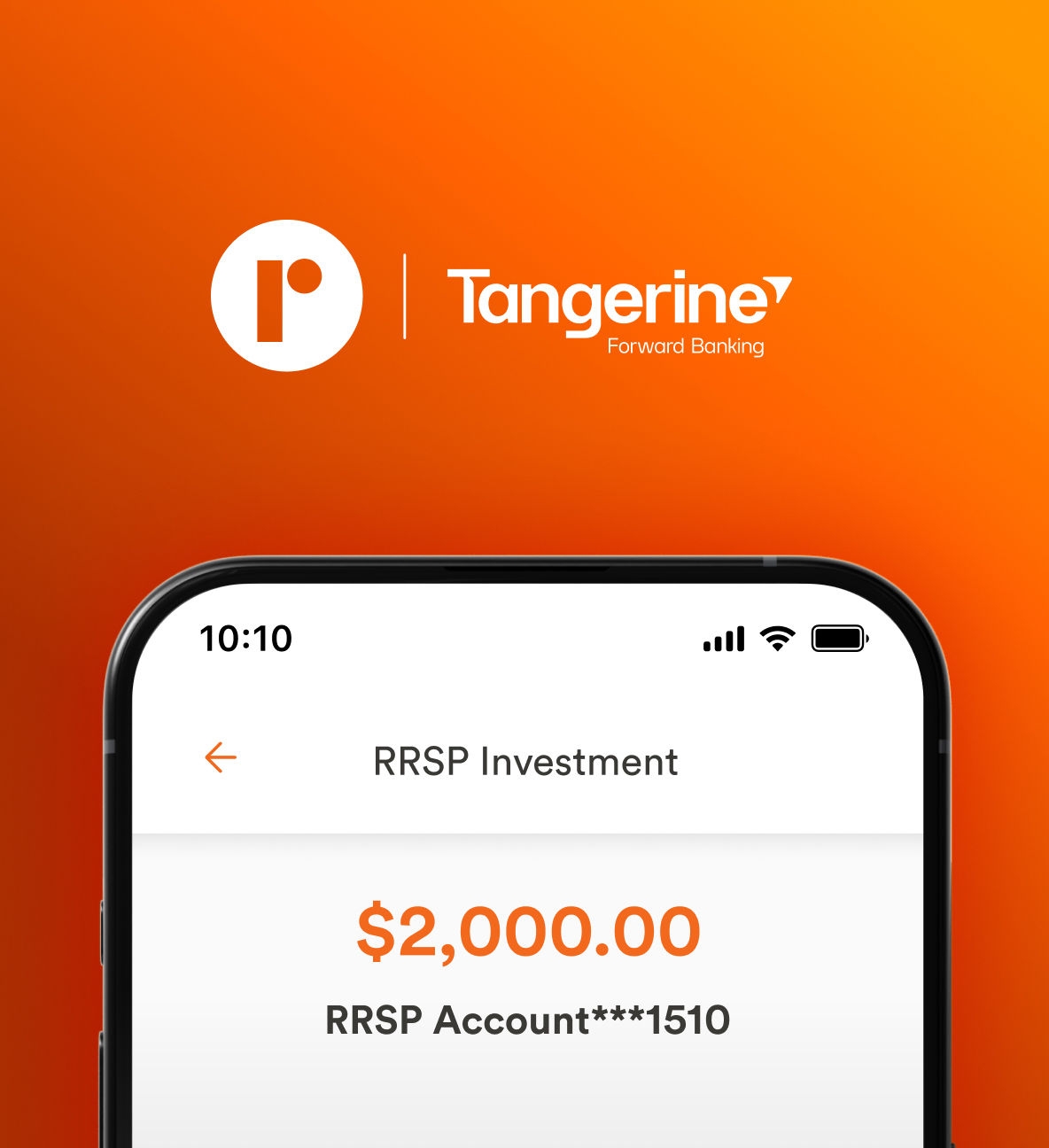

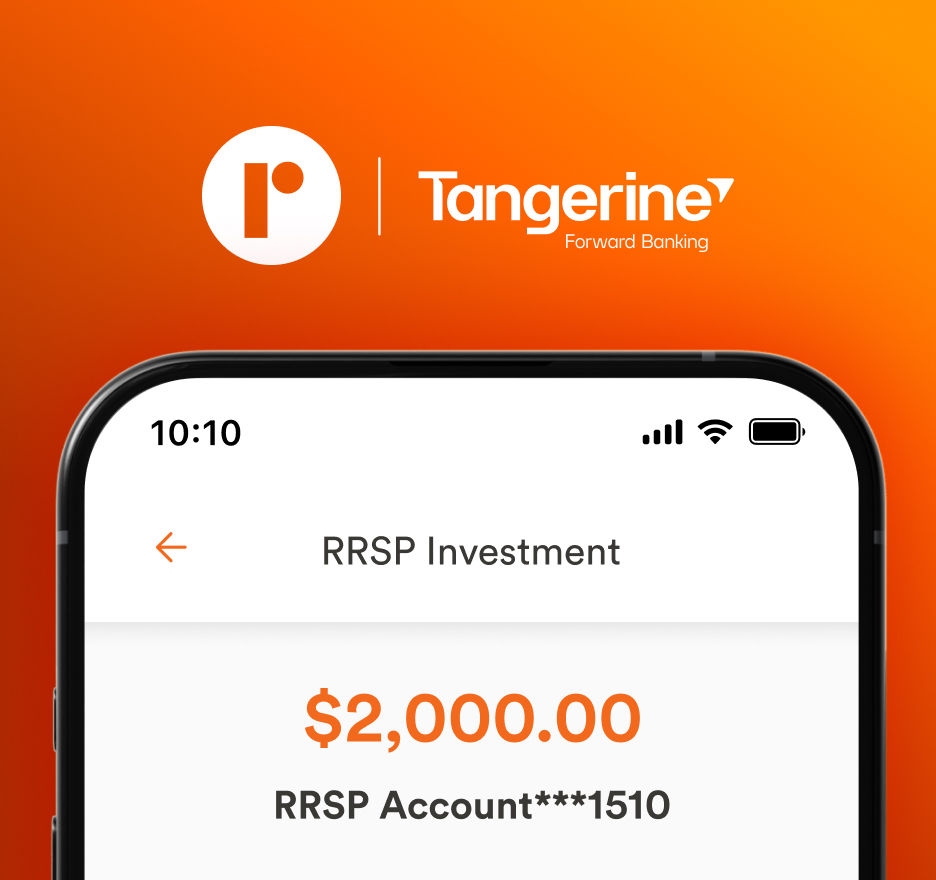

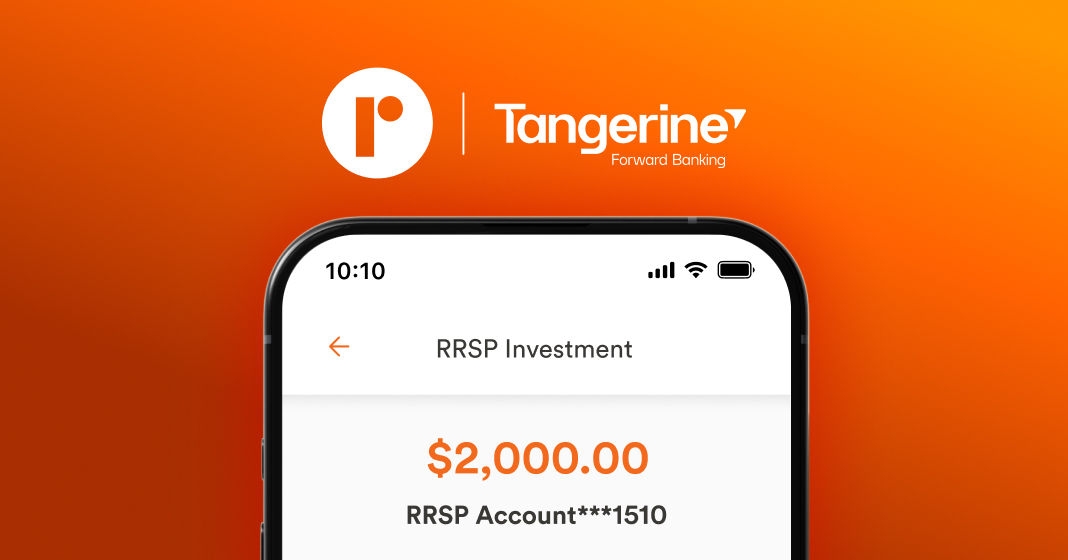

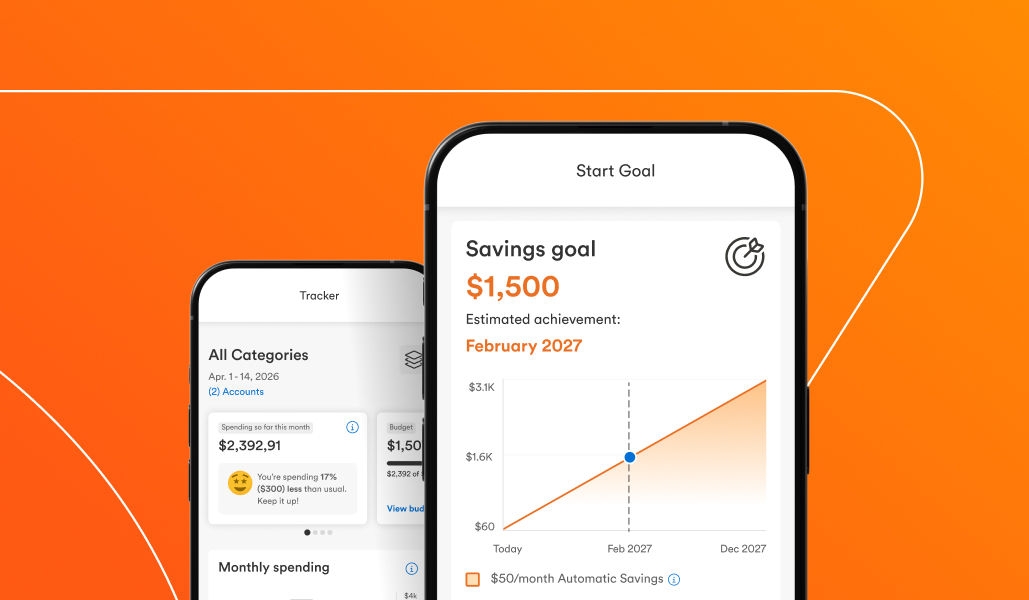

Build momentum with a [[NCO.SAVINGS_RSP.RATE]] boost²

THE JUICE ARTICLE

FINANCIAL CALCULATORS & TOOLS

Highlights

Special Offer

Get a hold of a new credit card and up to $600* in value.

THE JUICE ARTICLE

FINANCIAL CALCULATORS AND TOOLS

Highlights

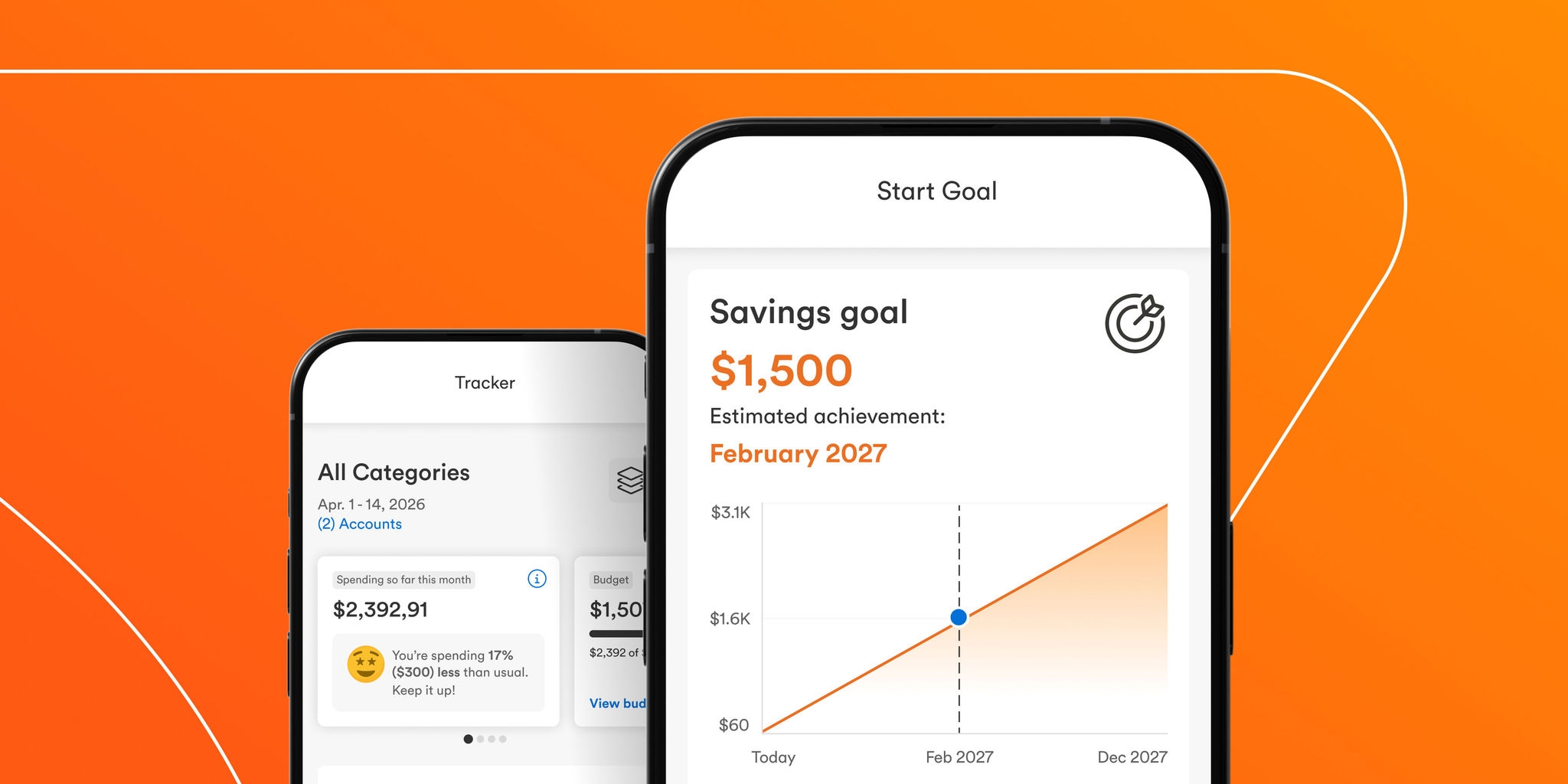

Earn up to a 3% bonus for your investments.‡‡

THE JUICE ARTICLE

FINANCIAL CALCULATORS AND TOOLS

Borrowing Options

Highlights

THE JUICE ARTICLES

FINANCIAL CALCULATORS AND TOOLS